Research003: DavidsTea (DTEA)

A neglected stock left for dead on a path to international growth

Disclaimer: I own shares in DTEA and may or may not continue to own it in the future. This article is not financial advice and I am not a qualified licensed investment advisor. All information written is for educational and entertainment purposes only and should not be used otherwise. Do your own due diligence or consult a licensed financial advisor before making any and all investment decisions. The items discussed are of my own views, ideas and opinions. All links included are for reference only and their respective organization is responsible for their content. I am not paid or sponsored for any of the ideas discussed.

Current Market Cap: $41 Million

Book Value: $46 Million

Enterprise Value: $33 Million

Valuation: ~$140 Million by 2025

What caught my attention:

DOMO Capital’s 13G Filing disclosing his 10% ownership of DTEA

The Segal family owns 45.43% of the company through Rainy Day Investments Ltd. (RDI)

Priced below book

No institution nor analyst covering the stock

Thesis

DavidsTea is in a growth stage after successfully completing their reorganization under Companies’ Creditors Arrangement Act (CCAA) September 2021. The Plan was approved June 17, 2021. This company is priced below book value and has zero debt. They are an asset light tea company shifting gears from expanding the number of retail stores pre-pandemic to expanding their Ecommerce and wholesale customers through their store-in-store concept. There are no significant institutional shareholders above 1% . No analyst has covered the stock since Q4 2017. DavidsTea is potentially a fast grower in a fairly slow growing industry, targeting at least 11% sales growth per year by 2025. The global tea market is expected to grow at 5.5% CAGR by 2025. This would imply almost $140 Million in sales. If their P/S ratio reaches 1, that would mean a 3.5x upside in the stock price in 3 years.

1. What is the intended destination for this business in ten or twenty years?

Their vision found in their SEC filings is to be the “World’s most innovative tea company.” In 10 years they would have; a few hundred signature tea blends, successfully expanded in the US and other countries through wholesale retailers, and have become one of the leading brands on Amazon selling online globally.

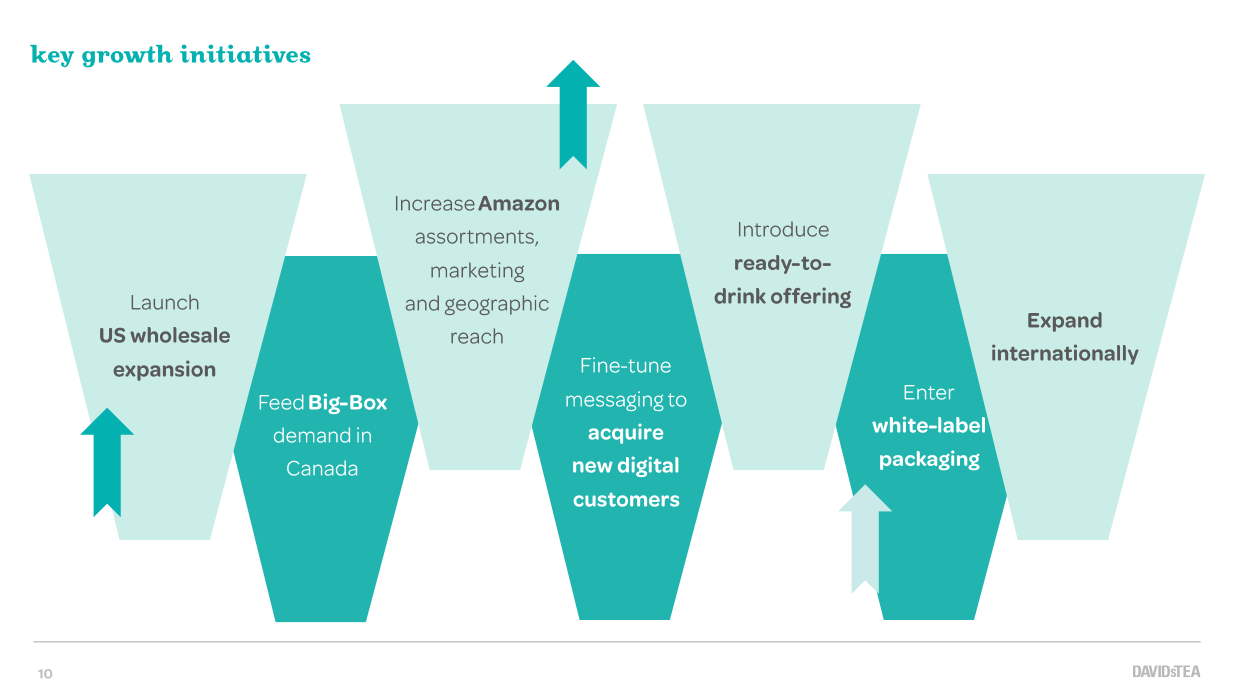

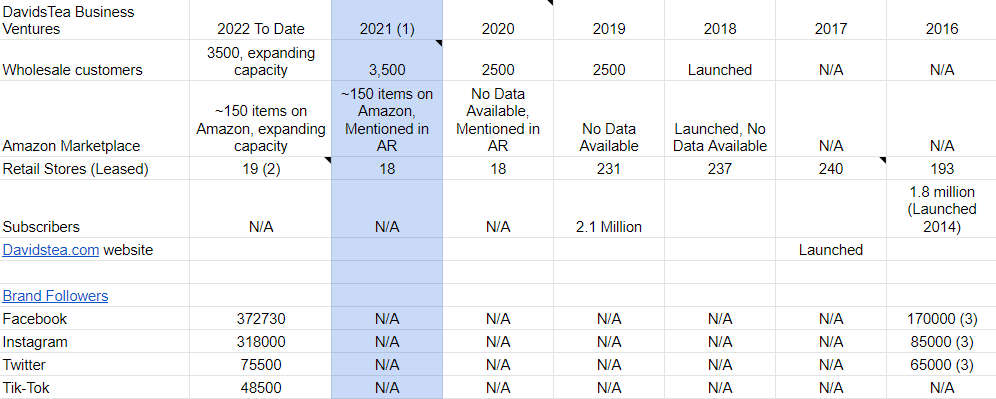

To start, the company’s five year plan is found in their investor’s presentation published June 15th, 2022. Their graphics sum up their strategy nicely. See select slides below. This foundational strategy if delivered profitably can allow them to scale quickly both domestically and internationally. They are making nice progress so far after expanding their wholesale retailers by 40% to 3,500 from 2,500 in 2021 from 2020, respectively. Their wholesale retailers include Rexall pharmacies, Loblaw groceries and pharmacies, and select Canada’s Costco and Walmart locations. Each of these wholesale retailers have significant room for expansion as covered by Value Digger from Seeking Alpha:

“The Rexall pharmacies in Canada are owned by McKesson (MCK), which covers the U.S., Canada and 12 countries in Europe. And in Europe, MCK serves more than two million people across more than 7,000 owned and banner retail pharmacies. On top of this, through its 97 pharmaceutical distribution centers, MCK delivers over 100,000 different essential medicines and supplies to more than 55,000 pharmacies and hospitals throughout Europe. Therefore, given that the relationship is already there, DTEA could make another deal with MCK expanding its wholesale segment internationally.”

Value Digger also covers three other optionalities for DavidsTea including, Rexall-like deals with other pharmacies including Walgreens and CVS, other brick and mortar retailers such as Barnes and Nobles, Hospitals, and THC-infused and/or CBD-infused teas with marijuana producers.

If their Costco and Walmart locations in Canada are a success, the company could easily scale into the US. To handle their fulfillment needs they’ve partnered with WIPTEC pick, pack&ship. This will help in their expansion with Amazon.com

A “brief” history from founding to $19 IPO to now ~$1.50/share

To understand where they want to go, it’s good to look at how they got here.

In 2008, David and Herschel Segal opened DavidsTea’s first retail store in Queen Street West, Toronto. In an interview with Business Insider from April 25th, 2011, before founding DavidsTea, David started a software business which failed. In search of another idea, he believed “there was a void in which we could deliver a fun, fashionable, and accessible tea experience on the main streets and in high traffic malls.” David with no retail experience sought Herschel’s (David’s cousin) help to co-found DavidsTea as Herschel had retail experience with Le Chateau. Herschel founded the clothing store in 1959. He was CEO until September 2006, and Chairman until February 2007. His wife, Jane Segal, took over as Chairwoman and CEO from 2008 through 2020.

By 2011, DavidsTea expanded to 40 locations in Canada, with 125 tea varieties, and 500 employees. David, the Brand Visionary of the company, attributes their rapid growth to “top quality product and the customer experience.” At the time David’s belief was “we find word of mouth most effective.” They didn’t focus on expanding their online marketing and instead focused on improving their current business model and opening new stores.

In 2014, Sylvain Toutant was appointed CEO and president of DavidsTea.

In June 2015, in the week of their IPO on Nasdaq, the shares traded as high as $27. They had expanded to over 136 Tea shop locations across Canada and 25 in the US, 150 tea varieties, and 2625 employees. Following their IPO, things began to go south with one bad news after another, despite revenue growth from 2015 to 2018 from USD $111 Million to $180 Million, respectively.

In 2016, David Segal left the company as Brand Ambassador to explore other entrepreneurial interests. It is unknown when, but sometime later he had sold his entire 10% ownership in DavidsTea. Later that year in October 2016, Sylvain announced his departure.

In 2017, Christine Bullen was named Interim President and CEO. On March 13, 2017 Joel Silver was named CEO. He had a nice track record of expanding retail and e-commerce revenues with Indigo Books & Music. Not even a year in, through an 8-k filing, Herschel sent a letter to the board on February 20, 2018 informing Rainy Day Investments Ltd. (RDI) began actively searching for a financial advisory firm to help take the Company Private.

The following month, March 5th, 2018, as mentioned in the same 8-k, Herschel stated his immediate letter of resignation as a director noting his disappointment with “the current divisions within the board.” He also expressed his thoughts on Joel, “We all hoped that the current CEO, who joined DavidsTea just over one year ago, would be able to implement the measures necessary to turn around the performance and results of the company. However, judging by the December results and the preliminary results since then, this is clearly not the case.”

On April 25, 2018, RDI announced it formally submitted seven new nominees for the board of Directors of DavidsTea. Herschel also accused that “[The current board] wants to sell it. [RDI] wants to fix [DavidsTea]. In response, three large shareholders including Porchlight Equity Management LLC, TDM Asset Management PTY Ltd., and Edgepoint Wealth management Inc. together owning 36.5% of the company “expressed serious concerns” over the plan.

Financial Post added some more light into the Proxy battle with comments from Joel and Segal. Some comments included Joel’s 3-year plan that included new-concept stores to solve the slow lines problem. Segal wasn’t “convinced a new store design is what the brand needs. He also sees room to improve the U.S. Business.”

On June 14, 2018 CEO Joel Silver resigned after Herschel won the Proxy fight “..to turf most of the existing board by electing seven nominees presented by the company's co-founder.” Segal became Chairman and Interim CEO. With the change in Management back to Segal, the company remained unprofitable and revenues still declined. They did show business growth in expanding through a wholesale retailer partnership with Loblaw’s grocery stores, and in 2019 Loblaw’s pharmacy locations.

Today, based on Tikr Terminal, none of the three large shareholders opposed to Herschel’s plan have ownership in the company.

On July 8th, 2020, due to Covid-19 and store closures, DavidsTea sought Bankruptcy Protection to reorganize their company under the Companies’ Creditors Arrangement Act (CCAA). On September 9th, 2021, they completed their restructuring, paying only $17.6 Million to its creditors. They shrank their retail base down to 18 flagship retail stores in Canada, closing 164 stores in Canada, and 42 in the United States.

On December 17th, 2020, Herschel’s Daughter Sarah Segal became CEO, while Herschel remained Chairman. On September 14th, 2021, Herschel announced his retirement and appointed his wife Jane Silverstone Segal as Director and Chair of the Board. Based on an interview in August 2022, Sarah and Herschel appear to work well together as Sarah mentioned she speaks daily with her father and that she “appreciate[s] his ideas and his retail experience.”

On June 2021, Their reorganization plan was approved and allowed DavidsTea to shed their physical retail stores and focus on their digital ecommerce business. DavidsTea now operates 19 retail stores in Canada, and has been leveraging other retail stores and ecommerce stores to grow their business. The amazing part, through all the chaos, they survived and kept significant ownership of their still existing business. DavidsTea is now practically a startup with an existing well known brand, capital light base, and a healthy balance sheet. As a side note Squish Candy, founded by Sarah Segal, followed the same reorganization path, shed all their retail stores and now is purely an ecommerce company. Sarah is no longer managing the company and is focused on DavidsTea.

The pandemic took a toll on all their retail businesses. From an outside perspective, the Segal Family made serious consolidations of all their businesses. This wasn’t the first time for Herschel Segal, as in the early days of Le Chateau when it nearly went bankrupt with four retail locations. Herschel stayed persistent nonetheless as he had many breakthroughs following the setback.

Since their reorganization, the company has been smooth sailing. No more management level drama, just focus on growth. Plus, their workplace was recently named “one of 2022’s Best Workplaces in Retail & Hospitality and 2021’s Best Workplaces Managed by Women.”

2. Who is management and what must management be doing today to raise the probability of arriving at that destination?

The brief history above shed some light to the Segal Family. The Segal Family is a family of founders. Herschel Segal founded Le Chateau and co-founded DavidsTea with David Segal. David Segal, no longer affiliated with DavidsTea, founded Mad Radish, a fast food franchise, and recently founded Firebelly’s Tea back in November 2021. Herschel’s wife, Jane Silverstone Segal, founded Oink Oink, a children’s store. Sarah Segal, now CEO and Chief Brand Officer of DavidsTea, founded Squish Candy.

Since becoming CEO Sarah has had only one interview. She is quietly building the company ignoring criticisms saying, “I’m not alone, I work with a very qualified team. I don’t pay too much attention to these comments. The results will speak for themselves.” That’s a characteristic of an Intelligent Iconoclast, building quietly ignoring outside noise.

What they must do

They’ll need to deliver on their plan. They’ll need to continue expanding, profitably, both domestically and internationally. It would be ideal to be more vertically integrated instead of partnering with other fulfillment companies. They also don’t need to continue to waste time with earnings calls either as no analyst is covering their stock. One earnings call per year is sufficient. As Sarah mentioned, “results will speak for themselves.”

Below is a crude spreadsheet tracking their progress.

(1) Post Reorganization with CCAA.

(2) They opened a new store in Montreal Eaton Center in January.

(3) 2016 Investors Presentation, Page 17.

3. What could prevent this company from reaching such a favorable destination?

There are a number of items that are unfavorable and could prevent DavidsTea from reaching their destination:

A common red flag is they have a history of one failed business and a series of huge setbacks. This could be another one unfolding slowly. For example, if they overpromise and underdeliver or if their strategy results in lower than anticipated returns.

They’ve been accused of nepotism. To counter argue, they’ve seem to have learned their lessons in giving management to other people as it’s now family operated. They must not have any more management drama to reach their destination. Note, the Segal family has yet to sell a single share of DavidsTea.

After David Herschel, the visionary co-founder left the company, the company has only gone south. If they don’t stay innovative or improve on their brand, the company could continue its southward trajectory.

Historically, this company has had fluctuating profitability, with recent years being unprofitable.

Their cash flow has also been fluctuating.

Even though this company is in growth mode, they aren’t vertically integrating as they are using WIPTEC pick, pack&ship to handle their fulfillment needs. This could hinder their growth and profitably.

If Herschel Segal or any family member loans to DavidsTea as Herschel has a history of supporting their family companies by providing loans with Le Chateau (and another $2.5 Million in 2017) and Squish Candy, that would be a huge red flag. It would be an early sign of another bankruptcy brewing.

I’ve yet to find a positive angle with Jane Silverstone’s management ability. If anyone knows a resource to study, I’m all ears.

Conclusion

To understand DavidsTea’s story, you have to understand what has happened so far (not recently) and who management is. DavidsTea went from family managed to other people managed back to family managed. The company grew quickly and rapidly when it was run by Segals. When the Segals handed management over to other people they experienced a multi-year long downturn filled with disagreements, high turnover, a proxy fight, media skepticism, and deteriorating share price. I’m Optimistically cautious with DavidsTea’s current progress. Historically, they have had periods of major growth and then significant contractions. Thus, I wonder how long-term an investor can stay invested in this company. For now, the storm seems to have passed, the business is still intact, they are being persistent, and are in growth mode. It will be good to keep tabs on this company’s progress.

Misc. Thoughts

From my twitter thread:

This stock resembles two of Peter Lynch's stock categories for a potential investment.

Excluding DOMO Capital (~10% owner), DavidsTea has close to 0% institutional ownership. More than 45% of the company is owned by the Segal family. The Last analyst joined on Q4 2017 for their earnings call. The Last analyst target estimate was on August 4th, 2018. It resembles the "The Institutions don't own it, and the analysts don't follow it" category.

According to Grand View Research, the global tea market is expected to grow at 5.5% CAGR by 2025. DavidsTea is targeting low double-digit growth per year by 2025. This would be at least double industry growth. In 2021, they increased their wholesale customers by 40%. This resembles “The Fast Growers”

I agree with this thesis but it needs one quarter of yoy growth. It hasn't had that in years.